Short answer: A retail roofer can add storm restoration on the strength of local trust — but the transition is harder and slower than the pitch. Ninety days gets you set up and legal to run your first claims; competency comes over your first full season. Plan for that, and do not bet the company on storm.

Know your lane: You document and price your own repair scope. You do not prepare, negotiate, or advise on the homeowner's claim unless you hold a public-adjuster license — that is regulated, and the rules vary by state. Verify yours before you train anyone.

Keep the mix: Do not go all-in on insurance work. Durable operators keep a large share of revenue in retail so a quiet hail year does not sink them — weigh that in storm chasing vs territory building, and the revenue math in the storm calculator.

Storm work is real and large. Severe convective storms drove more than $50 billion in U.S. insured losses for three straight years, and hail alone is up to 80% of that. NOAA counted 17 severe-storm billion-dollar disasters in 2024.

When one hits your territory, the question is whether you can serve your own customers or watch out-of-town crews do it. But most "add storm in 90 days" advice skips the part that actually decides whether you make money.

The insurance claim runs on rules and documentation you never needed in retail, and the failure mode is rarely a bad roof — it is a mishandled claim, a stripped supplement, or a cash-flow crunch nobody planned for.

This is the honest version: what the work requires, what gets paid, what breaks, and how to start without torching the reputation your retail business runs on.

Next Step

Turn the storm pivot into a training plan

A retail team cannot move into storm work with retail-only talk tracks. Start with the insurance, adjuster, and objection drills reps need before volume hits.

Know the Line You Cannot Cross

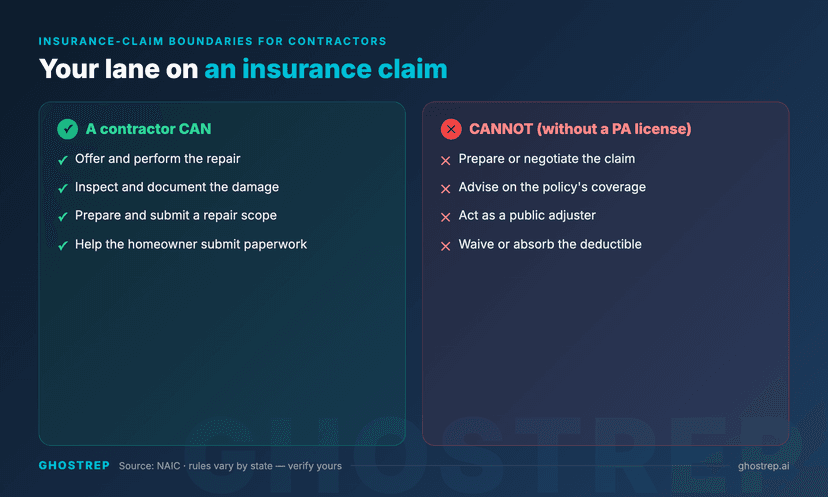

Start here, because getting it wrong can cost you your license. Homeowners get confused about who does what, and it is tempting to offer to "handle everything." In most states you legally cannot.

Per the National Association of Insurance Commissioners, in most states a contractor may not act as a public adjuster without a public-adjuster license. Without one, you cannot prepare the homeowner's claim, negotiate it with the carrier on their behalf, or advise them on what their policy covers.

Here is the nuance other contractors blur, so learn it precisely. Documenting and pricing your own repair scope — the shingles, the code items, the overhead and profit on the work you are doing — is your lane.

Taking over the homeowner's claim, arguing coverage, or signing an assignment of benefits to control the settlement is public adjusting. Price your work; do not adjust their claim.

Two rules that protect your license: Never offer to waive, discount, or absorb a homeowner's deductible — that is insurance fraud in most states. And because these statutes vary, verify your state's public-adjuster and solicitation rules before you train a single rep.

How the Claim Actually Works

You do not adjust the claim, but you have to understand it cold — the homeowner will ask, and your confidence here is most of your credibility. Here is the sequence on a typical replacement-cost policy.

| Stage | What happens | Your job |

|---|---|---|

| Homeowner files | They open the claim with their carrier | Nothing — the claim is theirs |

| Adjuster inspects | The carrier's adjuster writes an estimate, often from aerial imagery | Inspect the real roof and document the full repair scope |

| First check (ACV) | Carrier pays actual cash value minus the deductible | Do the work |

| Depreciation released | Carrier releases recoverable depreciation (RCV minus ACV) | Submit completion photos and affidavits |

One catch that changes the homeowner's out-of-pocket math: on an ACV-only policy, that depreciation is not recoverable at all.

What Actually Gets a Supplement Paid

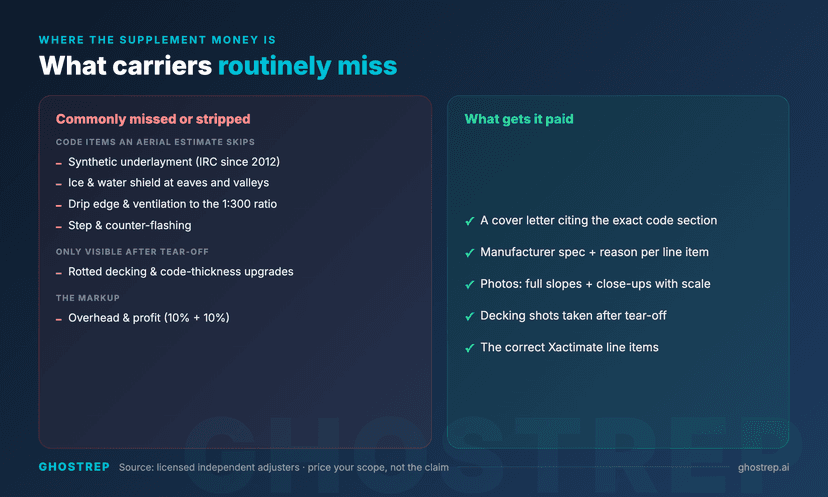

Because that first estimate is often written from satellite imagery, it routinely misses code-required and hidden items. Documenting those in your repair scope is where the real skill — and the real money — is. Independent adjusters who write these estimates say the same items get missed on nearly every claim:

- Code items an aerial estimate skips: synthetic underlayment (IRC code since 2012), ice-and-water shield at eaves and valleys, drip edge, and ridge-plus-intake ventilation sized to the 1:300 ratio.

- What only appears after tear-off: rotted or delaminated decking, step and counter-flashing, and decking-thickness upgrades current code requires.

- Overhead and profit — 10% plus 10% — routinely stripped even when the job genuinely coordinates three or more trades.

What separates a two-week approval from a six-week fight is not persistence — it is the cover letter. The supplements that get paid cite the exact code section, the manufacturer spec, and the reason for each line item, backed by photos: full slopes, close-ups with a scale reference, and decking shots taken after tear-off.

The ones that get denied skip the cover letter, cite no code, or make the classic own-goal — picking the wrong Xactimate line item, like three-tab on an architectural roof, and leaving thousands on the table.

Build your scope language with the roofing supplement script tool, and study how independent adjusters document these items so your scope reads in the language they approve.

Document It So an Adjuster Can't Argue

Retail work runs on a handshake. Insurance work runs on evidence, and that evidence has a grammar adjusters read.

Shoot every slope wide and close, timestamped and tied to the address. Chalk a test square and count impacts the way an adjuster does. Photograph the soft metals — gutters, downspouts, vents, flashing, AC fins, window screens — because hits there corroborate a real hail event.

If you want documentation a carrier cannot wave off, get HAAG-certified. HAAG is the hail-and-wind damage-assessment authority both contractors and adjusters train under, and a HAAG report is hard to dismiss.

Worth knowing: the residential certification requires 100 inspections as the primary inspector before you can even sit for it — a fair signal of how many real reps this work takes, and why 90 days makes you operational, not expert.

Next Step

Support the storm workflow after the inspection

Storm jobs break when documentation, supplement language, and homeowner follow-up are inconsistent. Give reps the field and operations assets that keep the claim moving.

What Breaks First in a Surge

When a real event hits, the crews are not what breaks first — the office is. Claims pour in faster than you can track them, paperwork turns to mush, and that is where wrong material orders, missed steps, and dropped follow-ups come from. Build the intake and tracking system before the storm, not during it.

Cash flow breaks next, and it is brutal. You buy materials COD while the first check — actual cash value minus the deductible — lags, carriers over-depreciate to shrink it, and recoverable depreciation only releases after you complete the work and submit completion photos and affidavits.

Supplements move the final number weeks later. Plan the float, or the surge that should make you money will strangle you instead.

The Honest Homeowner Conversation

A homeowner after a storm is nervous and half-expecting to be hustled, because plenty of contractors hustle them. The gap between sounding like a chaser and sounding like the local pro is specific:

| Sounds like a chaser | Sounds like the local pro |

|---|---|

| "We'll handle everything with your insurance" | "I document and price the roof; you and your insurer handle the claim" |

| "We'll get you a free roof" | "You may not have enough damage for a claim — I'll tell you either way" |

| Offers to cover or eat your deductible | Explains ACV, depreciation, and the deductible up front |

| Pushes an assignment of benefits to run the claim | Leaves the claim in the homeowner's hands |

Tell them the truth even when it costs you — the company that says "you may not have a claim" is the one they call next time. Drill that honest version in Role Play, and use Echo to hear how the calls actually go.

How to Actually Start

Ninety days is enough to get set up and legal, not to get good. Spend it on the boring foundation:

- Confirm your state's public-adjuster and solicitation rules in writing.

- Stand up your documentation and claim-tracking systems.

- Learn the claim mechanics and the code items above cold.

- Drill the honest homeowner conversation before a claim is live.

Then start where you are trusted — past customers in previously hit areas — so your first real claims are low-pressure reps, not cold doors.

When you do go wider, canvass only the confirmed-damage neighborhoods, pull a solicitation permit where your jurisdiction requires one, and lead with who you are — tighten the opener with the canvassing script generator, and follow up on a real cadence, because storm leads go cold fast.

Be honest about the first season. It will be rough: you will under-document a roof, get a supplement stripped, and hit a slow adjuster.

The operators who make it are not the ones who avoid that — they are the ones who do not quit after the first denied supplement, keep their retail base carrying the lights, and treat every early claim as training. Fix the gap, run the next one better, and by season two you have a system.

Your advantage is being the local name, so protect it. Document honestly, price your own scope and stay out of the homeowner's claim, never touch a deductible, and verify your state's rules before you run a single one.

Then drill the insurance conversation in Role Play before the next event — so when hail hits your territory, your own customers call you first.

Next Step

Compare storm opportunity against lead waste

Storm work can create a fast revenue window, but only if the team can capture, qualify, and follow up before competitors take the neighborhood.

Frequently Asked Questions

Do I need a special license to do insurance restoration work?

Your standard contractor's license covers the roofing work, but adjusting or negotiating the claim on the homeowner's behalf is public adjusting, which most states require a separate license for. Document and price your repair scope, leave the claim to the homeowner and their insurer, and verify your state's rules.

Why do supplements get denied?

Usually because they skip the cover letter, cite no code section, or use the wrong Xactimate line items. Supplements that get paid document each added item with the code reference, manufacturer spec, and photos — including decking shots taken after tear-off.

How is getting paid different from retail work?

The carrier pays actual cash value minus the deductible first, then releases recoverable depreciation only after the work is done and documented — often 30 to 60 days out, with supplements moving the number later. That slow, two-stage cash flow is why you keep a strong retail base.

How do I compete with storm chasers?

Not on their terms. Compete on being the licensed, local, still-here-next-year company that documents honestly and follows the rules, and never match an illegal offer like waiving a deductible. Homeowners choosing help for a claim value trust over a too-good pitch.

Storm deployment needs both coverage and economics. Compare the field canvassing platforms, then model each territory with the door-knocking ROI calculator and include the fully loaded cost of the rep.

Retail demand requires a different diagnosis: check the website conversion funnel before buying more traffic. If the team supplements demand with marketplaces, compare Angi and HomeAdvisor on cost per sold job; if it needs coaching technology, use the GhostRep–Siro comparison.

Free storm sales resources

Make storm-season training usable in the field

Use free tools for inspection summaries, follow-up language, adjuster prep, and objection handling before the next appointment hits.

Field sales tools

Build inspection summaries, homeowner updates, and post-appointment follow-up assets.

Browse field sales tools →Training tools

Use training tools for claim scripts, rebuttals, canvassing language, and storm-specific prep.

Browse training tools →Echo

Coach reps live during door knocks, inspections, and follow-up conversations when storm volume spikes.

See Echo →About the Author

Tim Nussbeck

Founder & CEO of GhostRep

Two decades in roofing—knocking doors, running teams, training 1,000+ reps. Built GhostRep to give every rep access to the coaching top teams get.

Storm-season next step

Turn storm-season advice into field execution

Use the field tools first if you need inspection summaries, homeowner updates, or follow-up language. Book a walkthrough if you want GhostRep mapped to storm-volume coaching.

- ✓Best fit if the issue is speed, consistency, and field execution.

- ✓Useful for inspection summaries, claim prep, and storm follow-up.

- ✓Demo shows how Echo supports reps when volume spikes and managers cannot be everywhere.

Start Here

Open storm-field tools

Build homeowner updates, inspection summaries, and follow-up assets for real appointments.

Open storm-field toolsNeed it mapped to your team?

Talk through your current workflow, traffic mix, and where GhostRep fits before you change anything.

Book a 15-minute walkthroughYou Might Also Like

Build an independent roofing estimate from field observations, scope, quantities, costs, assumptions, and review gates without crossing claim boundaries.

Read article →Compare HailTrace storm data with GhostRep sales coaching. HailTrace shows where to knock; GhostRep helps reps win the conversation at the door.

Read article →Compare storm chasing vs territory building ROI for roofing companies: profit, attribution, pipeline visibility, referrals, and long-term territory value.

Read article →